Social Security COLA 2026: What a 3.2% Increase Means for You

Social Security COLA 2026: What a 3.2% Increase Means for Your Monthly Payouts

As we look ahead to 2026, millions of Americans relying on Social Security benefits are eagerly anticipating the next Cost-of-Living Adjustment (COLA). The Social Security Administration (SSA) typically announces these adjustments in the fall, but projections and analyses often provide valuable insights into what beneficiaries can expect. Current estimates suggest a potential Social Security COLA 2026 of around 3.2%. While this is a projection and not a final figure, understanding its potential impact is crucial for effective financial planning.

This comprehensive guide will delve into the intricacies of the Social Security COLA 2026, explaining how these adjustments are calculated, what a 3.2% increase could mean for your monthly payouts, and how it fits into the broader economic landscape. We’ll explore the historical context of COLA, its purpose, and the challenges it aims to address, such as inflation and maintaining purchasing power for retirees and other beneficiaries. Whether you’re already receiving benefits, planning for retirement, or simply interested in the future of Social Security, this article will provide you with the knowledge you need to navigate these important changes.

Understanding the Social Security COLA: Its Purpose and Calculation

The Cost-of-Living Adjustment (COLA) is a critical component of the Social Security program, designed to ensure that the purchasing power of Social Security benefits is not eroded by inflation. Without COLA, the fixed dollar amount of benefits received by retirees, disabled workers, and survivors would gradually lose value over time, making it harder for beneficiaries to meet their daily expenses. The primary goal of the Social Security COLA 2026, like all previous adjustments, is to help beneficiaries keep pace with rising costs of goods and services.

The calculation of the COLA is tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, the SSA compares the average CPI-W for the third quarter (July, August, and September) of the current year with the average CPI-W for the third quarter of the last year a COLA was enacted. The percentage increase between these two periods determines the COLA. If there’s no increase, or if the CPI-W decreases, there is no COLA. This method ensures that the adjustment directly reflects changes in the cost of living experienced by a significant portion of the population.

For the Social Security COLA 2026, the SSA will look at the CPI-W data for July, August, and September of 2025. This data will then be compared to the CPI-W from the third quarter of 2024 (assuming a COLA was enacted for 2025). The resulting percentage, if positive, will be the COLA applied to benefits starting in January 2026. It’s important to remember that the 3.2% projection is based on economic forecasts and current inflation trends, which can fluctuate significantly before the official announcement.

Historically, COLA percentages have varied widely, reflecting different economic periods. There have been years with no COLA and years with substantial increases, particularly during periods of high inflation. These adjustments are not arbitrary; they are a direct response to economic realities, aiming to provide a safety net for those who depend on Social Security. Understanding this mechanism is the first step in comprehending the significance of the upcoming Social Security COLA 2026.

Projected 3.2% COLA for 2026: What it Means for Your Monthly Payouts

A projected 3.2% Social Security COLA 2026 would translate into a tangible increase in monthly benefits for all recipients. To put this into perspective, let’s consider some hypothetical scenarios based on average benefit amounts. While individual benefits vary widely based on earnings history, claiming age, and other factors, understanding the average impact can provide a clearer picture.

As of late 2024, the average Social Security retirement benefit for an individual is approximately $1,900 per month. If a 3.2% COLA were applied to this amount, the monthly benefit would increase by roughly $60.80, bringing the new average to approximately $1,960.80. For a couple receiving average benefits, say around $3,000 per month, a 3.2% increase would add about $96 to their combined monthly income, totaling $3,096.

These figures, while illustrative, highlight the direct financial impact of the Social Security COLA 2026. For many beneficiaries, especially those on fixed incomes, even a seemingly small percentage increase can make a significant difference in their ability to cover essential expenses such as food, housing, utilities, and healthcare. It helps to offset the rising costs they have likely experienced throughout the year.

It’s also crucial to consider the maximum Social Security benefit. For those who earned the maximum taxable amount throughout their working lives and claimed benefits at their Full Retirement Age (FRA), the impact of the Social Security COLA 2026 will be proportionally larger. For example, if the maximum benefit were around $3,800, a 3.2% increase would add approximately $121.60 to their monthly check, bringing it to about $3,921.60. These increases, while welcome, must also be viewed in the context of ongoing inflation and other economic factors that influence the overall financial well-being of beneficiaries.

The Broader Economic Context: Inflation and Purchasing Power

The Social Security COLA 2026 doesn’t exist in a vacuum; it’s a direct response to broader economic forces, primarily inflation. When the cost of living rises, the value of a fixed income diminishes. COLA aims to counteract this erosion, allowing beneficiaries to maintain their purchasing power. However, the effectiveness of COLA in fully achieving this goal is a subject of ongoing debate among economists and policymakers.

The CPI-W, while a widely used measure, might not perfectly reflect the spending patterns and cost increases experienced by seniors and other Social Security beneficiaries. For instance, healthcare costs, which often consume a larger portion of a senior’s budget, tend to rise faster than other goods and services included in the general CPI-W. This discrepancy can mean that even with a COLA, some beneficiaries might still feel a squeeze on their budgets, especially if their personal inflation rate exceeds the official COLA percentage.

Furthermore, the Social Security COLA 2026 will also need to be considered alongside other potential adjustments, such as Medicare Part B premiums. These premiums are often deducted directly from Social Security benefits. A significant increase in Part B premiums can offset a portion of the COLA increase, reducing the net gain for many beneficiaries. This interplay between COLA and Medicare premiums is a critical factor in assessing the true financial impact of the adjustment.

The overall economic outlook for 2025 leading into 2026 will undoubtedly shape the final COLA figure. Factors such as energy prices, food costs, housing market trends, and global supply chain stability all contribute to the inflation data that feeds into the CPI-W calculation. A 3.2% projection suggests that economists anticipate a continued, albeit potentially moderating, level of inflation. Beneficiaries should monitor these economic indicators closely as the official COLA announcement approaches.

Historical COLA Trends and Future Projections

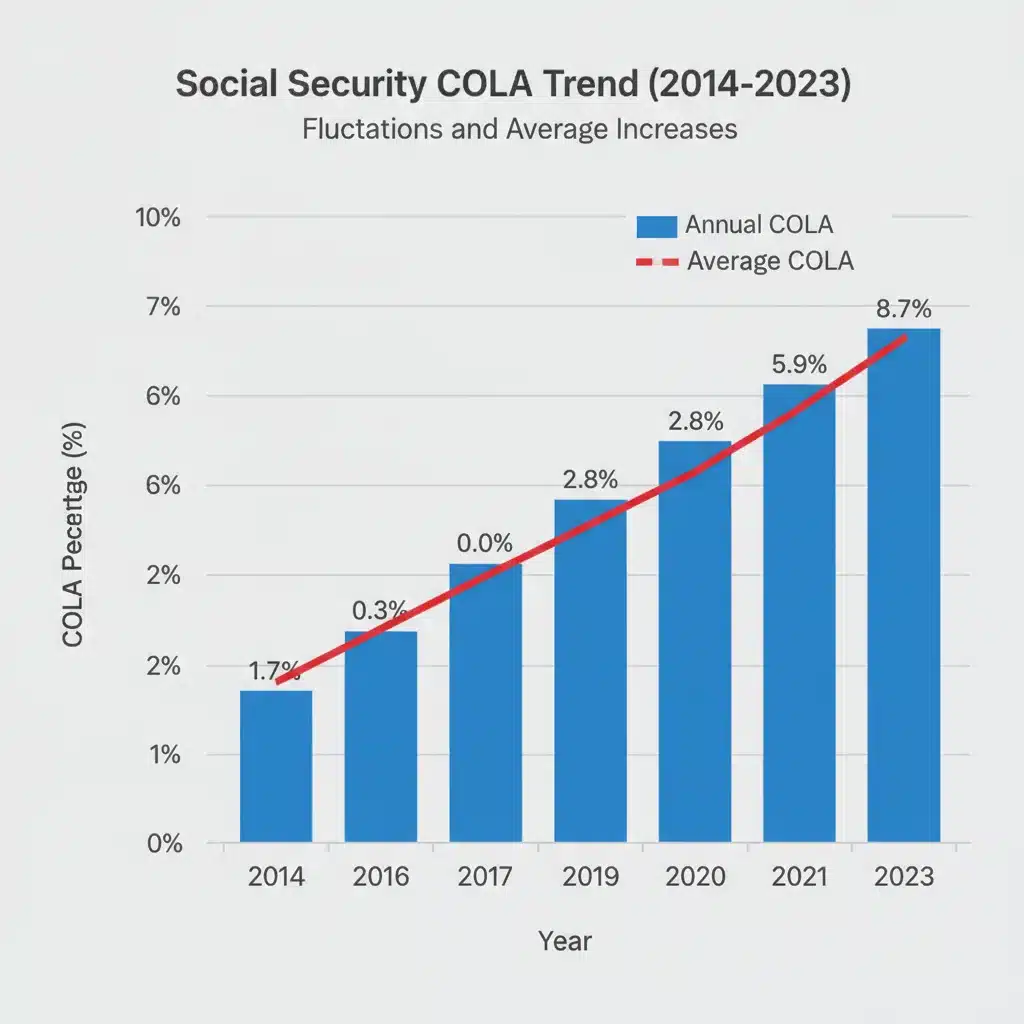

Examining historical COLA trends provides valuable context for understanding the projected Social Security COLA 2026. In recent years, COLA percentages have fluctuated considerably. For instance, 2022 saw a significant 5.9% increase, followed by an even larger 8.7% in 2023, reflecting a period of high inflation. The COLA for 2024 was 3.2%, which aligns closely with the current projection for 2026. These variations underscore the dynamic nature of economic conditions and their direct impact on Social Security benefits.

Years with high inflation typically result in higher COLA percentages, as the adjustment mechanism kicks in to protect purchasing power. Conversely, periods of low inflation or deflation can lead to very modest or even zero COLA increases. The absence of a COLA, while rare, has occurred in the past, such as in 2010, 2011, and 2016, during times of economic stagnation or very low inflation.

Forecasting the Social Security COLA 2026 involves making assumptions about future inflation rates. While current projections lean towards 3.2%, these are subject to change. Economic models consider various factors, including global economic growth, central bank policies, and geopolitical events, all of which can influence inflation. Beneficiaries and financial planners often look at reports from organizations like the Congressional Budget Office (CBO) or independent economic forecasters for insights into these projections.

Understanding these trends helps in long-term financial planning. While the Social Security COLA 2026 offers a direct increase, it’s part of a larger picture. Beneficiaries should consider how these adjustments, alongside other income sources and expenses, will impact their overall financial stability in retirement. It emphasizes the importance of not solely relying on Social Security for all retirement income but rather viewing it as a crucial component of a diversified financial strategy.

Strategies for Maximizing Your Social Security Benefits

While the Social Security COLA 2026 will provide an automatic increase, there are proactive steps individuals can take to maximize their Social Security benefits. These strategies often involve decisions made long before retirement, but some can still be implemented closer to or during retirement.

1. Work Longer and Increase Earnings

Social Security benefits are calculated based on your 35 highest-earning years. Working longer, especially if you’re in your peak earning years, can replace lower-earning years in your benefit calculation, thereby increasing your average indexed monthly earnings (AIME) and ultimately your benefit amount. This strategy can have a more significant impact than a COLA alone, as it raises your base benefit before any adjustments like the Social Security COLA 2026 are applied.

2. Delay Claiming Benefits

Perhaps the most impactful strategy for increasing your monthly payout is to delay claiming Social Security benefits beyond your Full Retirement Age (FRA), up to age 70. For each year you delay past your FRA, your benefits increase by a certain percentage, known as Delayed Retirement Credits. These credits can add significantly to your monthly check, making the impact of any future Social Security COLA 2026 even greater on a larger base amount. For example, if your FRA is 67, delaying until 70 could increase your monthly benefit by 24% (8% per year).

3. Understand Spousal and Survivor Benefits

If you are married, divorced, or widowed, you may be eligible for spousal or survivor benefits based on your current or former spouse’s earnings record. These benefits can sometimes be higher than your own, and understanding the rules for claiming them can significantly boost household income. Coordinating claiming strategies with a spouse can also optimize combined benefits, ensuring you make the most of the Social Security COLA 2026 and subsequent adjustments.

4. Monitor Your Earnings Record

Regularly check your Social Security earnings record through your online my Social Security account. Errors can occur, and correcting them ensures that your benefit calculations are accurate. Any discrepancies could lead to a lower base benefit, which would then diminish the effect of any COLA, including the Social Security COLA 2026.

5. Consider Tax Implications

While COLA increases your gross benefit, a portion of Social Security benefits may be taxable depending on your combined income. Understanding how your other income sources interact with Social Security and potential tax liabilities is crucial for assessing your net monthly payout. A higher Social Security COLA 2026 could, for some, push them into a higher income bracket where a larger portion of their benefits becomes taxable.

The Future of Social Security and COLA

The long-term solvency of the Social Security program is a frequent topic of discussion, and it naturally impacts perceptions of future COLA adjustments. While the program is currently able to pay 100% of promised benefits, projections from the Social Security Trustees indicate that without legislative changes, the trust funds may only be able to pay a reduced percentage of scheduled benefits in the coming decades. This outlook doesn’t directly affect the calculation of the Social Security COLA 2026, which is based on current inflation, but it does highlight the broader context of the program’s financial health.

Potential reforms could include adjustments to the COLA calculation method, such as switching to an alternative inflation index like the CPI-E (Consumer Price Index for the Elderly), which some argue better reflects the spending patterns of seniors. Such a change, if enacted, would alter how future COLAs, beyond the Social Security COLA 2026, are determined and could lead to different benefit increases.

However, for the foreseeable future, the current COLA mechanism remains in place, providing an essential safeguard against inflation for millions of beneficiaries. The annual adjustment, including the anticipated Social Security COLA 2026, is a testament to the program’s commitment to maintaining the purchasing power of its recipients. Staying informed about legislative discussions and economic forecasts is key to understanding the potential long-term trajectory of Social Security benefits.

How to Stay Informed About the Official 2026 COLA Announcement

While the 3.2% projection for the Social Security COLA 2026 offers a strong indication, it is not the final word. The official COLA announcement is typically made by the Social Security Administration in October of the year preceding the adjustment. For the 2026 COLA, this means the announcement will be made in October 2025, after the release of the CPI-W data for July, August, and September.

Beneficiaries can stay informed through several reliable sources:

- Official Social Security Administration Website: The SSA’s website (ssa.gov) is the most authoritative source for the official COLA announcement and detailed information.

- Social Security Statements: Each year, beneficiaries receive an updated Social Security Statement that details their new benefit amount, including any COLA applied.

- Reputable Financial News Outlets: Major financial news organizations and reputable retirement planning websites will widely report on the official COLA announcement as soon as it’s made.

Being aware of the official announcement date and knowing where to find accurate information will ensure you have the most up-to-date figures for your financial planning regarding the Social Security COLA 2026.

Conclusion: Preparing for the Social Security COLA 2026

The projected 3.2% Social Security COLA 2026 represents a vital adjustment designed to help beneficiaries cope with the rising cost of living. While not a final figure, this projection provides a valuable benchmark for individuals to consider in their financial planning. For millions, this increase will offer a much-needed boost to their monthly income, helping to maintain their purchasing power in an ever-changing economic environment.

Understanding how COLA is calculated, its historical context, and its interaction with other financial factors like Medicare premiums is essential. Furthermore, taking proactive steps to maximize your benefits, such as delaying claiming or understanding spousal benefits, can significantly enhance your financial security in retirement, making the impact of adjustments like the Social Security COLA 2026 even more beneficial.

As the official announcement approaches in October 2025, staying informed through reliable sources will be key. The Social Security COLA 2026 is more than just a number; it’s a reflection of economic realities and a critical lifeline for many Americans. By being prepared and informed, beneficiaries can better navigate their financial futures and ensure their Social Security benefits continue to support their needs.