Inflation Outlook 2026: Protect Your Savings from 3% Annual Rate

Inflation Outlook 2026: Protecting Your Savings from a Projected 3% Annual Rate

The economic landscape is constantly evolving, and understanding future trends is paramount for effective financial planning. As we look towards 2026, one of the most critical factors influencing personal and national economies will undoubtedly be inflation. Current projections suggest an Inflation Outlook 2026 with a potential annual rate of around 3%. While this might seem like a modest number, its cumulative effect on your savings and purchasing power can be substantial over time. This comprehensive guide will delve into the intricacies of the Inflation Outlook 2026, explore its implications, and, most importantly, equip you with actionable strategies to protect and even grow your savings in such an environment.

Understanding the Inflation Outlook 2026: What Does 3% Mean for You?

Inflation, in simple terms, is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. A 3% annual inflation rate means that something costing $100 today would cost approximately $103 next year. While this shift might feel incremental in the short term, its long-term impact on your accumulated wealth is significant. For instance, if your savings account yields less than 3% interest, you are effectively losing purchasing power each year. Over a decade, a 3% inflation rate can erode a significant portion of your savings’ real value. Understanding this fundamental concept is the first step in formulating a robust strategy for the Inflation Outlook 2026.

The Driving Forces Behind the Inflation Outlook 2026

Several macroeconomic factors contribute to inflationary pressures. For the Inflation Outlook 2026, we can anticipate a confluence of global and domestic influences. Supply chain dynamics, which have been a persistent issue in recent years, could continue to exert upward pressure on prices. Geopolitical events, energy price fluctuations, and shifts in global trade policies are also significant contributors. Domestically, factors such as wage growth, consumer demand, and government fiscal policies play a crucial role. Central bank monetary policies, particularly interest rate decisions, are designed to combat inflation, but their effectiveness can be limited by other underlying forces. Keeping an eye on these indicators will provide valuable insight into the evolving Inflation Outlook 2026.

The Erosion of Savings: Why Proactive Measures are Essential for Inflation Outlook 2026

Many individuals rely on traditional savings accounts for their financial security. However, in an environment of 3% inflation, these accounts often fail to keep pace. The interest rates offered by most savings accounts are typically lower than the inflation rate, leading to a real loss in value. This phenomenon is often referred to as the ‘inflation tax’ on your savings. Imagine having $10,000 in a savings account earning 1% interest. After one year with 3% inflation, your $10,000 would grow to $10,100, but the purchasing power of that $10,100 would be equivalent to approximately $9,800 in today’s money. This highlights the critical need for proactive financial strategies to counter the effects of the Inflation Outlook 2026.

Who is Most Affected by the Inflation Outlook 2026?

While inflation affects everyone, certain demographics are particularly vulnerable. Retirees and those on fixed incomes, for example, often find their purchasing power diminishing rapidly as the cost of living increases. Young savers, who have fewer years to compound their wealth, also face challenges if their initial savings are eroded by inflation. Moreover, individuals with substantial cash holdings or those heavily invested in low-yield assets will feel the pinch more acutely. Understanding your personal exposure to the Inflation Outlook 2026 is the first step in building resilience.

Strategic Approaches to Protect Your Savings from the Inflation Outlook 2026

Protecting your savings from a projected 3% annual inflation rate requires a multi-faceted approach. It’s not about finding a single magic bullet, but rather implementing a combination of strategies tailored to your financial situation and risk tolerance. The goal is to ensure your assets not only maintain their value but ideally grow beyond the rate of inflation. Here are some key areas to focus on:

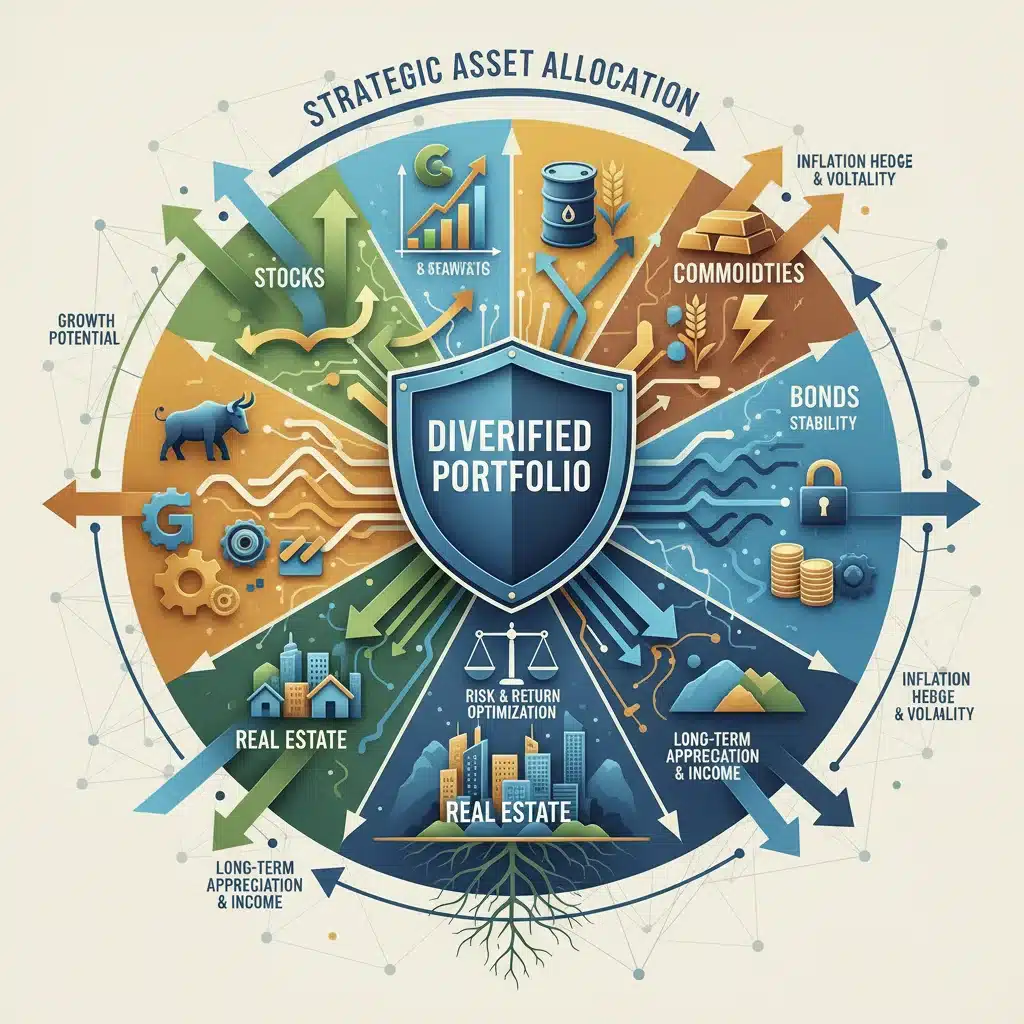

1. Diversify Your Investment Portfolio

One of the most fundamental principles of investing, and particularly crucial in an inflationary environment, is diversification. Spreading your investments across various asset classes can help mitigate risk and maximize returns. For the Inflation Outlook 2026, consider assets that historically perform well during inflationary periods.

Inflation-Resistant Assets to Consider:

- Real Estate: Historically, real estate has been a strong hedge against inflation. Property values and rental income tend to rise with inflation, providing a tangible asset that appreciates over time. Investing in real estate, whether directly or through Real Estate Investment Trusts (REITs), can be a powerful strategy.

- Commodities: Raw materials like gold, silver, oil, and agricultural products often see their prices increase during inflationary times. Gold, in particular, is often considered a safe haven asset. Investing in commodity-focused ETFs or futures can offer exposure.

- Treasury Inflation-Protected Securities (TIPS): These are government bonds designed to protect investors from inflation. Their principal value adjusts with the Consumer Price Index (CPI), ensuring your investment keeps pace with rising prices. TIPS are a direct and reliable way to counter the Inflation Outlook 2026.

- Stocks of Companies with Pricing Power: Look for companies that can easily pass on increased costs to consumers without significantly impacting demand. These often include companies in essential sectors or those with strong brand loyalty.

- Dividend Stocks: Companies that consistently pay and grow dividends can provide a steady stream of income that can help offset inflation’s effects.

2. Re-evaluate Your Budget and Spending Habits

In an inflationary environment, careful budgeting becomes even more critical. Understanding where your money goes is the first step to identifying areas where you can optimize spending and free up capital for investments that beat inflation. The Inflation Outlook 2026 demands a disciplined approach to your personal finances.

Practical Budgeting Tips:

- Track Your Expenses: Use budgeting apps or spreadsheets to meticulously track every dollar spent. This will reveal patterns and potential areas for reduction.

- Prioritize Needs vs. Wants: Differentiate between essential expenses and discretionary spending. In times of rising prices, cutting back on non-essential items can significantly improve your financial standing.

- Seek Value: Look for ways to get more value for your money. This could involve buying in bulk, utilizing coupons, or opting for generic brands where quality is comparable.

- Automate Savings: Set up automatic transfers to your investment accounts. This ensures you consistently save and invest before you have a chance to spend.

3. Maximize Your Earning Potential

One of the most direct ways to combat inflation is to increase your income. If your earnings grow faster than the inflation rate, your purchasing power actually increases. For the Inflation Outlook 2026, consider active steps to boost your earning capacity.

Income-Boosting Strategies:

- Negotiate Salary Increases: Regularly assess your market value and be prepared to negotiate for higher compensation. Highlight your contributions and research industry benchmarks.

- Acquire New Skills: Invest in yourself by learning new skills that are in demand. This can lead to promotions, new job opportunities, or higher-paying freelance work.

- Start a Side Hustle: Consider developing a side business or taking on freelance work to generate additional income streams.

- Invest in Your Education: Further education or certifications can significantly enhance your earning potential over the long term.

4. Consider Debt Management Wisely

Debt can be a double-edged sword during inflation. While fixed-rate debt (like a traditional mortgage) can become cheaper in real terms as inflation erodes the value of future payments, variable-rate debt (like credit card debt or adjustable-rate mortgages) can become more expensive as interest rates rise in response to inflation. The Inflation Outlook 2026 calls for careful debt assessment.

Debt Strategies for Inflation:

- Prioritize High-Interest Debt: Focus on paying down high-interest variable-rate debt as quickly as possible to avoid escalating costs.

- Refinance Fixed-Rate Debt: If interest rates are still relatively low, consider refinancing fixed-rate debt to lock in favorable terms, especially if you anticipate rates to rise further.

- Avoid Unnecessary New Debt: Be cautious about taking on new debt, especially if it’s for depreciating assets or has a variable interest rate.

5. Review Your Retirement Plans and Long-Term Investments

Inflation has a profound impact on long-term financial goals, especially retirement planning. The money you save today for retirement will have significantly less purchasing power in 20, 30, or 40 years if not properly managed. The Inflation Outlook 2026 is a good reminder to review your long-term strategy.

Retirement Planning in an Inflationary Era:

- Increase Contributions: If possible, increase your contributions to retirement accounts (401(k)s, IRAs) to offset the erosion of value by inflation.

- Invest for Growth: Ensure your retirement portfolio is adequately diversified and invested for growth, focusing on assets that have historically outpaced inflation. Don’t be overly conservative if your time horizon is long.

- Consider Annuities or Inflation-Adjusted Pensions: Explore options that offer inflation protection, such as certain types of annuities or pensions that adjust for cost of living.

- Consult a Financial Advisor: A professional can help you tailor a retirement plan that accounts for the Inflation Outlook 2026 and your individual circumstances.

The Role of Government and Central Banks in the Inflation Outlook 2026

While individual strategies are crucial, it’s also important to understand the broader economic context. Government fiscal policies (spending and taxation) and central bank monetary policies (interest rates, quantitative easing/tightening) play a significant role in shaping the Inflation Outlook 2026. These institutions aim to maintain price stability, but their actions can have various effects.

Fiscal Policy and Inflation

Government spending can inject money into the economy, potentially stimulating demand and contributing to inflation. Tax policies can also influence consumer spending and business investment. For example, large infrastructure projects funded by government spending could boost demand for materials and labor, pushing prices up. Conversely, fiscal austerity measures could dampen demand and help curb inflation. Keeping an eye on government budget projections and policy statements can offer clues about the future Inflation Outlook 2026.

Monetary Policy and Inflation

Central banks, like the Federal Reserve in the United States, use monetary tools to manage inflation. Raising interest rates, for instance, makes borrowing more expensive, which can slow down economic activity and reduce inflationary pressures. Conversely, lowering rates can stimulate the economy. The challenge for central banks is to strike a delicate balance: control inflation without triggering a recession. Their decisions will be pivotal in shaping the actual Inflation Outlook 2026.

Staying Informed: Key Indicators for the Inflation Outlook 2026

To effectively navigate the economic environment leading up to and during 2026, it’s vital to stay informed about key economic indicators. These metrics provide insights into inflationary trends and help you adjust your strategies as needed.

- Consumer Price Index (CPI): The most widely used measure of inflation, tracking the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

- Producer Price Index (PPI): Measures the average change over time in the selling prices received by domestic producers for their output. This can be an early indicator of future consumer inflation.

- Core Inflation: CPI and PPI often have ‘core’ versions that exclude volatile food and energy prices, providing a clearer picture of underlying inflationary trends.

- Wage Growth: Significant and sustained wage growth can contribute to inflation as businesses pass on higher labor costs to consumers.

- Interest Rates: Monitor central bank interest rate decisions and bond yields, as these reflect expectations about future inflation and economic growth.

- Commodity Prices: Fluctuations in the prices of key commodities like oil, gas, and agricultural products can directly impact inflation.

Conclusion: Proactive Planning for the Inflation Outlook 2026

The projected 3% annual inflation rate for 2026 is a call to action for anyone concerned about their financial future. While inflation is a natural part of economic cycles, ignoring its impact on your savings can have severe consequences. By understanding the forces at play, diversifying your investments, optimizing your budget, enhancing your earning potential, and managing debt wisely, you can build a robust defense against the erosion of your wealth.

Remember, financial planning is an ongoing process. The Inflation Outlook 2026 serves as a reminder to regularly review your strategies, stay informed about economic developments, and adapt your approach as circumstances change. Proactive measures taken today will undoubtedly pay dividends in protecting your savings and ensuring your financial security tomorrow. Don’t let inflation silently diminish your hard-earned money; empower yourself with knowledge and strategic action.